Automotive pressure plates remain essential in clutch-based drivetrains, even as automatic transmissions and electric vehicles change long-term vehicle architecture. A pressure plate applies clamp load to the clutch disc, supports torque transfer between the engine and transmission, and helps manage heat at the friction surface. Its role is especially important in manual vehicles, light commercial vehicles, hybrids, two-wheelers, and repair-intensive internal-combustion fleets.

The Global Automotive Pressure Plates Market size was valued at USD 4.6 billion in 2025 and is estimated at USD 4.75 billion in 2026. The market size is expected to grow to USD 5.55 billion by 2032, with the market to register a CAGR 2.72% during 2026-32. This points to moderate expansion, supported more by replacement cycles than rapid new-fitment growth.

Replacement demand remains the strongest support base

Pressure plate demand is closely tied to vehicle age, clutch wear, repair economics, and service-channel availability. As internal-combustion vehicles remain in operation for longer, clutch assemblies move into higher-mileage replacement cycles. According to S&P Global Mobility, the average age of U.S. light vehicles reached 12.8 years in 2025, showing how aging fleets continue to enlarge the repair pool.

This directly supports Global Automotive Pressure Plates Market growth because pressure plates are rarely replaced in isolation. When a clutch disc wears out or release performance deteriorates, workshops often replace the pressure plate, clutch disc, release bearing, and related hardware together. Since gearbox removal is labor-intensive, complete clutch repair helps reduce repeat-labor risk and improves customer confidence.

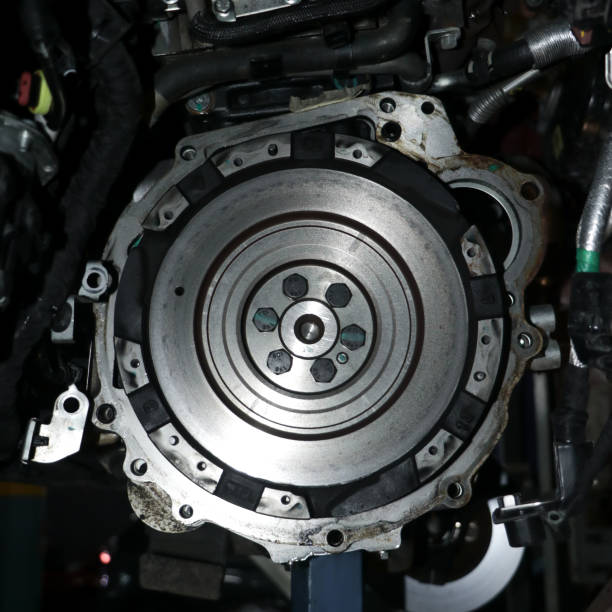

Diaphragm pressure plates lead through fitment and serviceability

Diaphragm pressure plate grabbed market share of 55%, making it the leading product type. The segment’s strength comes from compact design, lower pedal effort, smoother release behavior, stable clamp load, and wide use across passenger cars and light commercial vehicles. These attributes make diaphragm designs suitable for mainstream repair and replacement applications.

Valeo Service explains that a standard clutch cover uses a diaphragm spring to provide clamp load and a pressure plate with enough mass to dissipate heat from the friction surface. This reinforces why the component is not basic hardware. It affects thermal management, engagement quality, drivetrain response, and clutch life.

The Global Automotive Pressure Plates Market trends also show a shift toward self-adjusting covers. These systems help compensate for lining wear and maintain more consistent release behavior through the service cycle. This makes advanced diaphragm pressure plates more valuable in premium repair kits and vehicles exposed to stop-start driving, higher torque loads, or frequent clutch engagement.

Single plate clutch remains the core clutch format

Single plate clutch grabbed market share of 50%, making it the leading clutch type. Its dominance reflects broad use in mainstream manual vehicles, cost-efficient design, easier repair understanding, and strong availability across independent workshops and aftermarket distributors.

Single plate clutch systems remain commercially relevant because they offer a practical balance between torque transfer, serviceability, packaging, and affordability. Multi-plate systems are important in motorcycles, performance applications, and compact high-torque designs, while heavy-duty clutch systems support trucks and commercial vehicles. However, single plate formats continue to lead where repair cost, parts availability, and workshop familiarity drive purchase decisions.

Schaeffler’s LuK RepSet positioning supports this service logic. The company identifies LuK RepSet as a manual clutch repair solution that includes a clutch pressure plate, clutch disc, and optional release bearing. This confirms how the aftermarket increasingly treats the pressure plate as part of a matched system rather than a standalone replacement component.

Transmission change is the main structural challenge

The main pressure on the market comes from the declining role of conventional manual clutch systems in new passenger cars. According to the U.S. Environmental Protection Agency’s 2025 Automotive Trends Report, manual transmissions have remained below 1% of production since model year 2021. This reduces new OEM fitment opportunities for traditional clutch pressure plate systems in some developed markets.

Electric vehicle adoption adds another constraint. According to the International Energy Agency, electric car sales topped 20 million globally in 2025, and one in four new cars sold worldwide was electric. Battery-electric vehicles typically do not require engine-to-gearbox pressure plate assemblies, which limits long-term demand in fully electric passenger vehicle platforms.

The market is therefore shifting rather than disappearing. Internal-combustion vehicles, hybrids, diesel platforms, light commercial vehicles, two-wheelers, and regional manual-transmission fleets continue to sustain service replacement. Suppliers that rely heavily on conventional manual passenger cars may face portfolio pressure, while aftermarket and commercial-vehicle channels remain more resilient.

Asia Pacific leads through production scale and repair density

Asia Pacific leads with a 40% share of the global market. The region benefits from large vehicle production ecosystems, extensive internal-combustion and hybrid vehicle parc, two-wheeler and light commercial vehicle use, and dense independent repair networks. This combination supports both original equipment fitment and long-term replacement demand.

India adds a relevant demand signal. According to SIAM, passenger vehicles posted their highest-ever sales in FY 2024-25 at 4.3 million units, while utility vehicles contributed 65% of total passenger vehicle sales. This matters because utility vehicles and light-duty platforms support broader drivetrain, clutch, and repair ecosystems, particularly in markets where internal-combustion vehicles remain central to mobility.

Self-adjusting technology improves repair quality

Product innovation is increasingly focused on service quality, not only basic clamp force. ZF Aftermarket states that the SACHS XTend clutch pressure plate provides automatic wear compensation by separating facing wear from diaphragm spring movement. This helps stabilize release behavior as the clutch lining wears, which can improve service life and pedal consistency.

Valeo also identifies self-adjusting clutch covers with a wear compensation system between the pressure plate and diaphragm. These systems support stronger engagement stability and reduce deterioration in pedal feel. For workshops, this reduces comeback risk after clutch replacement and supports higher-value repair kits.

This technology direction supports the Global Automotive Pressure Plates Market forecast because replacement demand increasingly favors OE-equivalent kits, self-adjusting covers, technician guidance, catalog accuracy, and better installation confidence. Product value is moving from commodity replacement toward system-level drivetrain restoration.

Competitive landscape remains moderately concentrated

More than 20 companies are actively engaged in producing automotive pressure plates, while the top 5 companies acquired around 40% of the market share. Eaton Corporation plc, F.C.C. Co. Ltd., Tieliu Co. Ltd. (Westlake), Schaeffler AG (LuK), Valeo Service SAS (Valeo), ZF Friedrichshafen AG (SACHS), EXEDY Corporation, AISIN CORPORATION, Setco Auto Systems Pvt Ltd (LIPE), Raicam Driveline S.r.l., Hubei Tri-Ring clutch Co. Ltd, Xlerate Driveline India Ltd., E. SASSONE Srl, Jiangxi Outaishi Auto Parts Co. Ltd., and RAM Clutches are among the listed companies.

Recent updates also reflect the service-led direction of the category. ZF lists SACHS XTend clutch pressure plates for passenger cars in its aftermarket clutch portfolio, while AISIN lists clutch cover technology with Hot Seating and Diaphragm Spring Turnover design in its aftermarket portfolio.

Conclusion

Automotive pressure plate demand is becoming more dependent on aging internal-combustion fleets, service replacement, complete clutch kits, and regional repair networks than on new manual passenger-car fitment alone. The Global Automotive Pressure Plates Market forecast remains supported by diaphragm pressure plates, single plate clutch systems, Asia Pacific’s repair density, and self-adjusting clutch technologies. Based on market data from Vyansa Intelligence, future performance will depend on aftermarket reach, kit-based replacement, commercial-vehicle service demand, and supplier ability to adapt to changing drivetrain architectures.