Natalie Donaldson, a military veteran, presents having a portrait during the their domestic bad credit installment loans California when you look at the Tulsa, Okla. An effective COVID direction system that was supposed to assist their particular stop foreclosure finished up increasing their unique home loan repayments from the fifty% each month. Michael Noble Jr./to have NPR hide caption

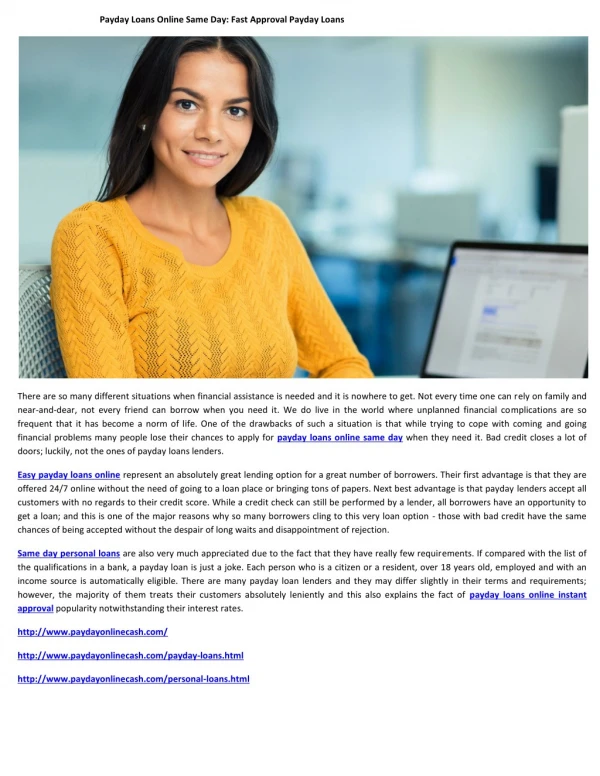

Once you walk-up in order to Natalie Donaldson’s nothing cottage-build household when you look at the Tulsa, Okla., you happen to be met of the their vibrant smile, along with her well-muscled pit bull terrier entitled Sigrid.

Donaldson is actually an army veterinarian, and she got a crude enter the newest military. She’s got PTSD. In fact it is partially as to why buying so it residence is important to their particular – this lady has her own place in which she seems secure.

Nevertheless these months Donaldson is scarcely in a position to scrape the cash to each other to expend their financial, since the she is harm by the an excellent botched Va mortgage program. The application form is meant to assist their particular, but alternatively it stranded their particular inside the an altered financial with an effective greater rate of interest who has got elevated their unique costs because of the 50% – almost $500 much more every month, forever.

“I purchased property which i you certainly will afford without any help and you can now I am unable to,” Donaldson told you. “The newest girl which is my personal mortgage advisor, she doesn’t have the power to complete some thing… with the exception of playing me personally rant and you can scream and let me know she’s sorry over and over again.”

NPR enjoys learned that thousands of other experts appear to have already been likewise damage because of the VA’s missteps and leftover stranded inside higher-cost mortgage loans. Considering files gotten within the Versatility of information Work, at the very least step one,300 veterans wound-up when you look at the funds one to raised the monthly obligations by more 50%.

A program to assist vets was damaging them

All of this come for Donaldson shortly after COVID hit. She would become being employed as a schoolteacher immediately following making new Military however, their pops is passing away and you will she necessary to stop working so you’re able to manage your.

Donaldson entitled their mortgage company, desperate for let. “I was sobbing and you may she goes, ‘Oh honey, exactly why are you weeping… it is probably going to be Okay.’ “

It has to were Ok, while the in those days Congress told you anyone with an excellent federally recognized financial you may pause their repayments for up to 18 months owing to what’s named a great COVID financial forbearance. Donaldson, including many almost every other experts, provides a home loan supported by new Institution off Veterans Items. Therefore she is told she could avoid spending their home loan.

It’s Pros Big date. The fresh new Va states it cannot let tens of thousands of vets they left stuck

A home loan forbearance gets a homeowner ways to briefly prevent paying its home loan, following when they return on their feet financially, these are generally allowed to be in a position to resume spending and get current on their mortgage. A beneficial forbearance isnt designed to produce a big raise in a beneficial homeowner’s mortgage repayment since entire part is to let a person who was struggling to shell out before everything else.

Natalie Donaldson served just like the an army police officer about Military. Like millions of other veterans she ordered property using a Virtual assistant home loan that’s backed by this new Institution off Pros Things. An effective fiasco inside Virtual assistant leftover tens of thousands of vets including their unique in danger of shedding their houses adopting the COVID pandemic strike. Michael Noble Jr./to have NPR hide caption

Once they come new forbearance, of many vets was indeed told if they certainly were willing to begin paying again, their overlooked payments might possibly be moved to the rear of the financing label. That would help them only restart and make the brand-new month-to-month mortgage repayment, additionally the missed costs would get paid back off the trail.